In the Oil Basics, we have a good picture of the oil types, products, and supply and demand sides. But how do oil prices change in the markets?

This is the second article in a series on oil markets. We will talk about the pricing of crude oil.

#How Oil Is Priced

There are two prices in the oil market: the spot price and the futures price.

The spot price is the current price for crude oil. It is the price for immediate delivery. The futures price is the agreed price for future oil delivery. In real life, futures prices are more commonly referenced than spot prices as they have a bigger impact on the oil market.

Let’s briefly talk about how oil futures contracts work. The contract will clearly state things like date of settlement or expiry, number of barrels of oil to be traded (typically 1000 barrels per contract), quality and type of oil to be traded, and method of settlement. Most oil futures contracts will not involve physical settlement as that requires taking or delivering the actual oil. Most people trade oil futures and profit by going short or long.

For the WTI and Brent oil prices we see on the news, it is always the futures price for the nearest contract, not the spot price. For example, WTI Crude (May’26) is the futures price for May 2026 delivery.

#What Moves Oil Prices

The futures price depends on what people think about the future, not the present. Now we know the spot price and the futures price — so what shapes those expectations? There are mainly four factors.

#Supply

First, the supply side. Production plays a huge role in oil prices as it directly determines how much oil is available.

-

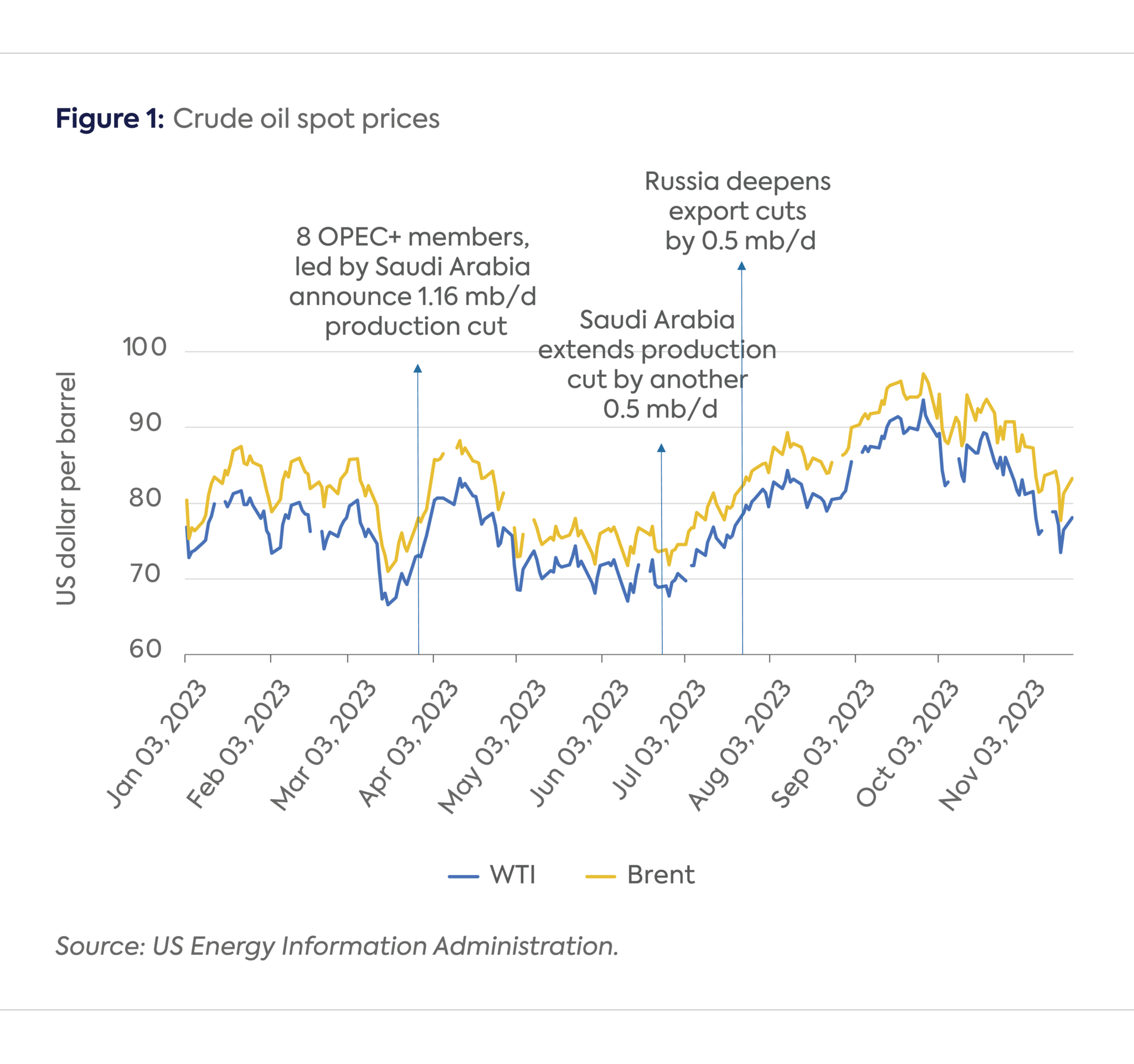

OPEC As we talked about earlier, OPEC produces about 35% of the world’s crude oil and accounts for 50% of all oil traded. Every single cut or increase decision will cause the price to rise or fall (as shown below).

For example, in April 2023, OPEC+ surprised markets with a voluntary cut of 1.16M bpd — Brent jumped from ~$73 to ~$87 within weeks.

Fig. 1: OPEC+ production decisions and their impact on oil prices

Fig. 1: OPEC+ production decisions and their impact on oil prices

-

US Shale Oil Besides OPEC, the US also plays a role in oil prices as the swing producer. Shale oil is cheaper and faster to drill than conventional oil, so it can add supply to the market more quickly.

During 2014–2016, US shale producers kept drilling despite falling prices, flooding the market and helping push Brent from over $100 to below $30.

-

Disruptions Regional conflicts can have a huge impact on oil prices, especially those that happen in or near oil-producing countries.

The 2019 drone attack on Saudi Aramco’s Abqaiq facility knocked out 5.7M bpd overnight — oil spiked 15% in a single day.

-

Spare Capacity Since oil prices are largely influenced by the future, people also look at extra capacity — how much more oil producers could pump but are choosing not to. If spare capacity is low, the market gets nervous about future supply, and the price rises.

In mid-2022, global spare capacity dropped to around 2M bpd (mostly held by Saudi Arabia), which was one reason oil stayed above $100.

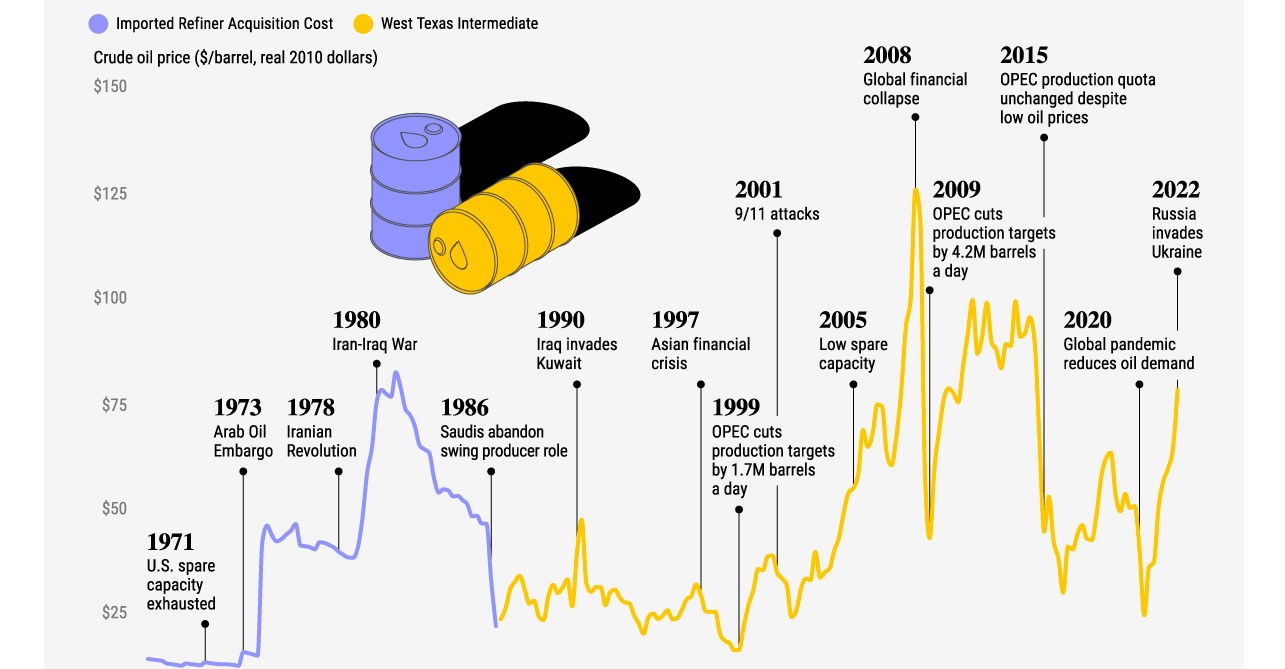

Fig. 2: Major events alongside oil prices

Fig. 2: Major events alongside oil prices

The chart above shows a holistic view of major events alongside oil prices. All four factors can change the price drastically.

#Demand

The supply side is indeed a strong factor in oil prices, but as we all know “demand and supply” — demand can be just as important.

-

Economic Growth When economic growth pushes GDP up, it certainly increases oil demand as more factories, shipping, and travel happen during economic expansion.

Among all countries, China, on its own, is the single biggest demand driver for oil prices as it is responsible for roughly 30% of global manufacturing output. As China’s GDP grows, more and more oil is imported. China’s crude oil imports have grown dramatically, rising from roughly 4–5 million barrels per day (bpd) in 2010 to a record 11.1 million bpd by 2024.

-

Seasonal Patterns Beyond long-term growth, oil demand also follows short-term cycles. Summer driving and winter heating drive oil prices up as well. Part of the reason for the 2025 summer oil price spike is seasonal demand.

-

Demand Destruction But demand does not just go up — it can also work in reverse. If the oil price gets too high, people will start to cut back on oil products, thus reducing the consumption and demand for crude oil. As a result, the oil price pulls back down.

#Inventories

Besides supply and demand, the amount of oil sitting in storage also sends a strong signal to the market.

-

Commercial Inventories Commercial inventories are oil stored by companies. When inventories are high, it signals oversupply — there is more oil available than the market needs, which pushes prices down. When inventories are low, it signals a tight market, and prices tend to rise.

In early 2020, COVID lockdowns crushed oil demand so fast that storage facilities around the world filled up. WTI futures briefly went negative in April 2020 because traders could not find anywhere to store the oil.

-

Strategic Stocks (IEA) The IEA (International Energy Agency) is a group of 32 member countries, mostly OECD nations like the US, Japan, South Korea, and Germany. It coordinates emergency oil responses, and every member must hold at least 90 days’ worth of net oil imports in strategic reserves.

In March 2026, as the Iran war pushed Brent toward $120, Trump ordered a 172 million barrel release as part of a coordinated IEA effort of 400 million barrels globally, helping pull prices back into the $90–$95 range.

#US Dollar

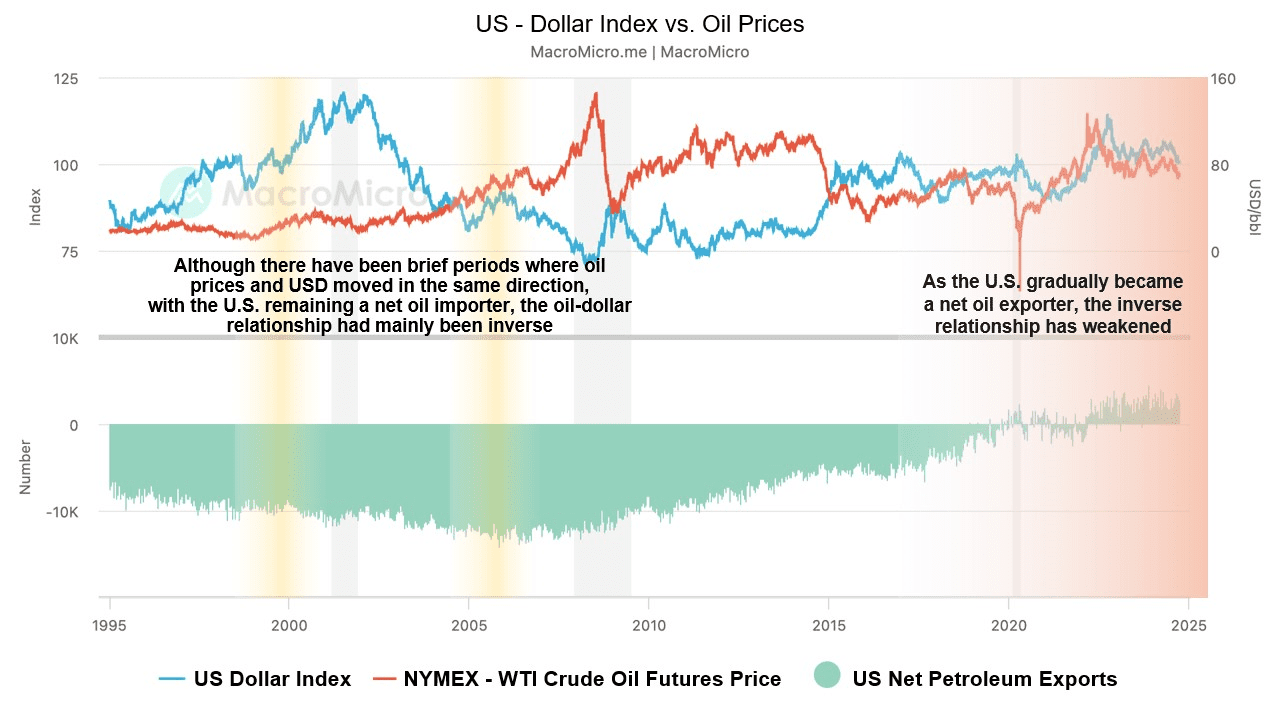

Oil is priced in USD globally — a system known as the petrodollar, which started with a 1974 US-Saudi deal. Because of this, the US dollar and oil prices have an inverse relationship: when the dollar strengthens, oil becomes more expensive for other countries to buy, which reduces demand and pushes prices down. However, as the US has gradually become a net oil exporter, this inverse relationship has weakened in recent years.

Fig. 3: USD and oil price inverse relationship

Fig. 3: USD and oil price inverse relationship

#Reading the Spreads

Now that we understand what moves oil prices, we can look at the relationship between different benchmarks — the spreads between them tell us a lot about what is happening in the market.

#WTI-Brent Spread

The spread is simply Brent price minus WTI price. Since Brent reflects international and seaborne oil (sensitive to Middle East disruptions, European demand, and shipping risk), while WTI reflects US domestic conditions (Cushing storage levels, shale production, and pipeline capacity), the gap between them reveals where the stress is.

- Spread widening (Brent >> WTI): an international supply disruption while US supply is fine.

- Spread narrowing (Brent ≈ WTI): calm global markets, or a crisis hitting everyone equally.

- WTI > Brent (rare): a US-specific supply issue. This happened in 2011 when shale oil backed up at Cushing with nowhere to go.

Right now we are seeing this in action. The Iran war and the closure of the Strait of Hormuz have disproportionately impacted international supply, pushing the Brent-WTI spread from its normal $5–$8 range to over $15 — its widest gap in over a decade. Brent surged past $114 while WTI stayed around $97, because US domestic supply remains largely unaffected while seaborne oil faces massive disruption.

#Dubai/Oman Premium

Dubai/Oman usually trades below Brent because it is medium-sour crude — the quality discount we talked about in Part 1.

But the US-Iran war flipped this: with the closure of the Strait of Hormuz, Dubai/Oman oil prices hit an all-time high, trading at a premium over Brent as Middle Eastern supply became the scarcest oil in the world.

Supply, demand, inventories, and the US dollar all push and pull on oil prices — and the spreads between benchmarks show us where the pressure is building. With the Iran war reshaping the market in real time, these are not just textbook concepts. In the next article, we will look at how the current conflict is impacting the oil market.